The whole sorry mess in one picture

Photo credit:

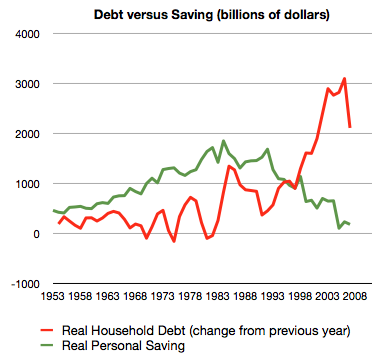

Philip Brewer How much money is there in the economy to borrow? Well, if you don't have foreigners lending you large amounts of money, and you don't have central banks creating large amounts of money, then the amount of money available to be borrowed each year is roughly equal to the amount of money saved.

Take a gander at that graph. The green line is personal savings. The Bureau of Economic Analysis calculates that. It's just income minus spending--the obvious way of figuring saving. The red line is debt. The Federal Reserve calculates that value. The value on the graph is the change from the previous year--that is, it shows each year's new debt, just like the green line shows each year's saving. Both values are adjusted for inflation--the graph is in billions of (year 2000) dollars.

Everything looks fine from the 1950s right up until the late 1990s. New borrowing goes up during expansions and drops during recessions. (Sometimes it even drops below zero in a recession--people are paying off old debt faster than they're taking on new debt.) Saving rises a bit during the early 1980s, when interest rates reached generational highs, then declines pretty steadily as interest rates fell.

Then, starting in about 1998, borrowing just goes through the roof.

How did that happen? It was largely due to two things:

- China and rich oil-producing countries were making huge profits from our purchases, leaving them with lots of dollars. One thing they did with those dollars was lend them to us.

- Banks lobbied for and got permission to lend much more money for each dollar deposited. Instead of lending out around $10 for each dollar deposited, they could lend out $30 or $40. And, using houses as collateral, they did just that.

Of course, none of this is news. People could have (and did) produce the same graph last year or the year before or the year before that--and when they did, they saw the same thing we see. So, why is it now that things have come to pieces? Starting back in about 2005, the American consumer reached the point that they could no longer service ever-increasing amounts of debt. That led to the housing bubble popping. The result is what you can see in the last datapoint on the graph--less new borrowing in 2007.

All the news just lately has been about how the banks have been unwilling to lend. Just as important, I think, is that consumers are unable to borrow--the ones who would be willing to take on more debt simply wouldn't be able to make the payments.

The real, long-term solution is going to have to be to get borrowing back under saving. That, though, would mean a huge decline in spending. Just the little drop in new borrowing that you can see on the graph is sending us into a recession. The central bank and the Treasury are terrified about what letting borrowing drop all the way down to our current level of saving would mean. So, since the consumer is all borrowed up, they're trying to have government borrowing replace consumer borrowing.

Because of their fear, the Treasury hasn't done one obvious thing that's necessary to get the economy back on sound footing--it hasn't made it more attractive for savers to save. They're afraid that more saving would mean less spending, resulting in an even worse recession. And yet, longer term, it's that saving that will support future borrowing.

In the meantime, we've dodged one bullet. Those folks who looked at versions of this graph from past years and got worried mostly figured that the crisis would come when China and the rich oil-producing nations either decided that they weren't comfortable loaning us so much money, or simply decided to spend more of the money on domestic consumption. Instead, the crisis has had the perverse effect of bringing dollars flying back to the US all the faster--brought by people who figure that US Treasury securities are the safest way to hold dollars.

That means that the Treasury has been able to borrow the hundreds of billions of dollars used for the bailout so far. But that's not the same thing as making sure that there's domestic savings to support domestic borrowing. Quite the reverse.

Disclaimer: The links and mentions on this site may be affiliate links. But they do not affect the actual opinions and recommendations of the authors.

Wise Bread is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to amazon.com.

{kind=link}

This chart is quite embarrassing to me. We are suppose to be the leading economy in the world and too many people are trying to cheat the system. Money is too easy to be made to try to make it illegally. All of this happened because banks started lending people money that they knew could not pay it back. Now everybody has to reap the benefits.

Excellent headline, excellent post. This bread is delicious!

Thanks for the great article! I'm so glad to have a voice of reason amongst all the craziness out there. My heart just dropped when I saw the treasury secretary on tv the other day recommending another "incentive" package. And the commentators are all trying to figure out how to encourage people to just spend it instead of use it to pay down debt. Don't they have a name for it when you keep doing the same thing and expecting different results, stupidity maybe?

I particularly appreciate your post.

...and about this part:

"The central bank and the Treasury are terrified about what letting borrowing drop all the way down to our current level of saving would mean. So, since the consumer is all borrowed up, they're trying to have government borrowing replace consumer borrowing.

Because of their fear, the Treasury hasn't done one obvious thing that's necessary to get the economy back on sound footing--it hasn't made it more attractive for savers to save. They're afraid that more saving would mean less spending, resulting in an even worse recession. And yet, longer term, it's that saving that will support future borrowing."

How do you feel about the Fed, the Treasury, and especially about the people who have been making the decisions on our economy, and on the welfare of the citizens...?

Are they doing their job? Is their job to protect the stock market and the investors, or to protect the people as a whole? When the people say they love their country... do they also love the way we empower our leadership?

Thanks for a clear and incisive commentary, Philip.

my opinion only

Wisebread has had some very common sense articles recently. Thanks and keep it up!

The government has tried to create $ 700B in liquidity and guaranteed another $ 1.4 trillion in interbank loans in an effort to create liquidity for the banks to make loans. However, the $ 700B was diluted by $ 125B used by the government to purchase equity in the banking system via the issuance of preferred stock. In theory there should be approximately

$ 2.0 trillion in new available funds for banks to loan. Sounds nice but they are using the maoney to shore up their weak capital positions so they can keep their doors open.

With the banks net interest margins shrinking due to a lack of cheap deposits (savings) to turn into loans the availability of funds is actaully decreasing.

The main incentive for people to save is to earn a higher interst rate or return on their money. Banks are not going to raise the rate of interest on their savings any time soon as it would increase their cost of funds and decrease their interest margins or their profits.

Makes it all very clear doesn't it. How on earth could a gov let that happen?

If we follow the recent advice of Warren Buffet, which in essence is to go against the popular opinion, then those of us who have been saving the past few years, like myself, are about to make out like bandits when deflation hits, and hits hard.

Rather than a huge drop in borrowing down to current savings levels, I believe we'll see a huge rise in savings, along with a decline in borrowing until the two are correlated more naturally as they were prior to 1998.

Since more and more people will be hoarding their cash, retailers are about to start slashing prices, especially with the slash happy holidays fast approaching.

Bargain hunting here I come! (I hope)

After having been primarily worried about inflation (based on money-supply growth and actual price increases), I wrote earlier this month about inflation going away for a while.

Even so, I'd be very leery of positioning my finances to expect just deflation. In just the past couple of months, the compound annual rate of growth in the monetary base surged from its normal range (where it would vary between -4% to 9%) to an utterly insane 140% or thereabouts. That portends a truly awesome amount of inflation that might come surging through the economy at any time.

Philip: I would add that not only is the graph instructive, but that you've written one of the most cogent explanations of what needs to happen that I've read anywhere - and I've been reading all kinds of financial blogs & articles on this topic all over the 'net for months now (over a year now, actually).

You hit the nail on the head: the problem is not lack of lending and borrowing. The problem is that people borrowed too much and saved too little. Instead of borrowing more $Billions from the likes of China to try to encourage banks to lend, we should be encouraging people to save again. Higher interest rates for savings would be a good place to start (which would mean higher interest rates in general). Perhaps the government could consider exempting the first $2000 of interest income from taxes?

Sorry, how is this the US government's fault? The current conservatives pride themselves on small government, compassionate conservatism, non-intervention and so on. They were voted in by Americans. And yet American voters re-supported sending billions of tax-payer dollars to rebuild an overseas country.

The USA is not a nanny state, where the government "looks after" the populace from cradle to grave. Sure the government has responsibilities, and the rest of America has "rights". But Americans collectively have responsibilities too.

American citizens, voters and populace did this to themselves. Through lack of vigilance, distractions, immediate gratification, conspicuous consumption etc.

I love America and Americans. But the sooner this is understood, and collective behaviour changes, the easier it will be to climb out of the ditch.

Hear phrases like tough love, cold turkey, weaning, sacrifice AND humility in the next few years.

Americans unite in the face of external enemies: the USSR, communists, resurgent Japan, Arabs, Iran, Al Qaeda; even "manufactured" enemies like "liberals", gays, the French, "old Europe" etc. Now, look at your national debt as an enemy, and attack it. Debt in moderation is a good thing. But not when it is that magnitude.

Attack political corruption. Attack waste. Attack the addiction to foreign oil. Attack the over-emphasis on wedge issues. Attack willful ignorance.

I am confident that Americans can maintain their individualism, and yet, pull together in a common-ish direction -- Upwards. I'm confident that Americans can gain satisfaction not from consumerism, but by gaining knowledge on the impact of their actions. I'm confident that America can convert it's metaphorical financial flab into muscle, and regain its own confidence in doing so.

America is at a critical juncture. Competitors are not standing still. Contrary to some ideas, the world largely views Americans favourably, and would love to see America regain strength. But the world will carry on, if America fades into irrelevance.

A rising tide lifts all boats, but only when you are above water.

Good Rant, CFOX...

I have the same general feelings about conspicuous consumption... but

I feel a little different about blaming government. I DO blame government... and the "FatCats".

Government operates in the shadows. 40,000 lobbyists hired almost entirely by business to influence 535 congressmen.

Political appointments based on friendship and not competence.

A government "by the people" based on a system designed for the 1700's. Electoral College, and the loss of the concept of "Confederation" which would empower the states.

Domination of the media by 5 or 6 collusive entities... and a failure of the anti trust laws. "The Mushroom Syndrome". ( Feed them lots of manure, and keep them in the dark.)

Today... Oct 24 may be the biggest Stock Market Day in history. Do we blame it on the people?...

Do we do it to ourselves? Maybe... but as to the question of how to change the system? To Vote? More likely anarchy, I think.

So while I don't disagree with the concept of personal responsibility, it begs the question... How?

my opinion only

There has been no point to being a saver over the last decade or more, at least here in the U.S.

Government policy has kept savings rates low because they wanted to subsidize borrowers.

If you did save, you saw the purchasing power parity of your savings cut nearly in half as the dollar devalued.

Deflation may occur in "toys" like consumer goods (electronics, vehicles, stainless-steel appliances)

But not in anything I want to buy like housing.

Few are willing to admit their house's value is no more than it was a decade ago, so most (non-distressed) "for sale" houses - don't.

While there has been huge growth in the money supply, little is being used (near zero velocity).

That will change, however, resulting in inflation at least as bad as the 1970s, if not close to South American levels.