Interview with AFFIL executive director Jim Campen

Photo credit:

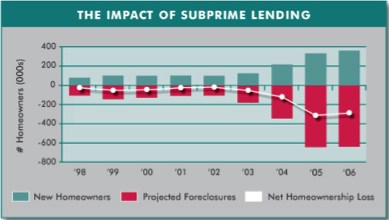

Center for Responsible Lending Early in the subprime lending collapse, Wise Bread posted a report from Americans for Fairness in Lending explaining how the subprime lending boom hurt everyone. Since it's a topic of considerable interest to Wise Bread readers, when AFFIL offered to make Jim Campen, their executive director, available to answer some questions, we jumped at the chance.

Wise Bread: One of the most obvious ways to avoid this sort of crisis in the future would seem to be better borrower education, to make them less vulnerable to predatory lending practices, and put them in a better position to make good choices. The section in your report on "Fixing the Problem," though, doesn't mention borrower education. Do you not see borrower education as useful in fixing the problem?

Jim Campen: Borrower education is absolutely key to healthy credit-lender activity. And that message is out there. The problem is, consumer education is often the only message out there – and, inherently, it blames the consumer for loans-gone-bad. Our job is to show the other side of the equation. We don’t want calls for financial education to divert attention from the industry reforms that we advocate. Few would argue that we should rely on consumer education so that people can protect themselves against toxic drugs; instead we have the FDA to regulate what kinds of drugs are available and we require prescriptions from licensed doctors, who have ethical and legal responsibilities toward their patients. Similarly, some toxic lending products and features should be banned and lenders should have ethical and legal responsibilities toward their borrowers.

Wise Bread: One of your proposals is to create incentives for investors who own bad loans to renegotiate them. With local lenders, those incentives were inherent in the system. Besides just the lack of a local connection, what else in the mechanics of securitization acts to reduce those incentives?

Jim Campen: There are are at least two such mechanisms. The first is that the legal documents which govern the trusts into which the mortgage loans are pooled to provide the backing for the securities often limit or prohibit the ability of trustees -- and thereby loan servicers -- to modify the terms of the loans in the trust. The second is that the foreclosure attorneys and others involved in the foreclosure process often receive little or no compensation for the substantial time and effort involved in working out a modification; their clear financial incentive is to proceed with foreclosure.

Wise Bread: Do you have any specific policy suggestions for restoring or replacing those incentives?

Jim Campen: Unlike some parts of the whole securitization business, this isn't rocket science. Those involved are smart enough to figure this out if they want to do so -- or are forced to do so One key is making sure that foreclosure attorneys and others involved in the foreclosure process have a financial incentive to spend the time and effort needed to bring about a loan modification or other solution when this is in the mutual interest of the borrower and the lender -- at a bare minimum the fees for accomplishing this should be considerably above the fees for facilitating a foreclosure.

Wise Bread: One of your proposals is that the government should help homeowners who are stuck in troubled loans. There are plenty of people out there who, when their neighbors were buying bigger houses, stayed in a small house or continued to rent--because they knew that they couldn't afford the bigger house. It seems especially unfair to come along now and ask these people to subsidize their neighbors who are living in houses that they can't afford. Do you think the benefits to the people in trouble, together with those for the neighborhood and community, outweigh the fairness issue?

Jim Campen: This is a legitimate concern. The issue here is how to help those who were harmed by unscrupulous, dishonest, or fraudulent lenders without "bailing out" those who were simply greedy or engaged in outright speculation. Helping those who were harmed by unfair lending is simply righting a wrong, and we don't see anything unfair about that. In the same way that it is appropriate to use public funding to get people into affordable housing, it is appropriate to use public funding to keep people from losing their homes as a result of predatory lending behavior.

Wise Bread: Why is that? We generally don't use public funding to rescue people who are harmed financially in other ways--victims of con games don't get public funding, nor do people who lose money to crooked gamblers. How is this case different, or would you support public funding for those cases as well?

Jim Campen: We as a society have decided that affordable homeownership is a public policy goal that it is worth using public resources to promote. If it is worth public money getting people into homes, then it is only logical that it is worth spending public money to enable them to stay there. Two additional arguments: (1) that governments bear a moral obligation to assist people because of governmental negligence in failing to offer adequate borrower protections, and (2) that foreclosures result in public costs on neighbors and local governments as well as private costs on borrowers. Government assistance to victims of crooked gamblers or other con artists is one of a very large number of issues which lie outside AFFIL's area of concern: abusive consumer lending.

Wise Bread: What forms could government support for homeowners with troubled loans take?

Jim Campen: Most of the legislative proposals for helping homeowners facing foreclosure do not involve direct financial assistance to the homeowners. Rather they are focussed on the provision of legal and/or credit counseling support. The demands on counseling agencies greatly exceed their current capacity; this capacity needs to be very substantially expanded. In addition, the provision of legal representation to borrowers who have legitimate claims to make against predatory lenders, but are either unaware of this or unable to afford a lawyer, is a legitimate form of government support (although the lending lobby will fight hard to prevent any such measure). In addition, legislation could provide necessary guidelines governing access to and use of the various funds that have been established to help borrowers in trouble.

Wise Bread: Although rising home prices benefit homeowners, flat--or even falling--home prices would benefit renters who would like to buy. Successful efforts to help homeowners with troubled mortgages stay in their houses would tend to delay any such adjustment in home prices. Do you see any way to help people with troubled loans (and their communities) that doesn't also have the effect of keeping homeownership out of the reach of many people of modest income?

Jim Campen: The kind of regulation that AFFIL supports would operate to moderate gyrations in the market that lead to extreme highs and lows in housing prices -- such as the recent housing price bubble and current subprime mortgage industry collapse. Fair lending regulation would result in fair lending products that make home ownership possible for people of modest income. The lower prices available are coming now are at great cost to communities. The tidal wave of irresponsible lending in recent years played a major role in sustaining the housing bubble, pushing house prices to excessive levels, and leading people into foreclosure. AFFIL's concern is for people who have been harmed by predatory lending and for the neighborhoods where predatory lenders have been particularly effective in pushing their toxic loans.

Disclaimer: The links and mentions on this site may be affiliate links. But they do not affect the actual opinions and recommendations of the authors.

Wise Bread is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to amazon.com.

{kind=link}