SBA Loans Up 90%

This article is a reprint of Wise Bread's contribution to OPEN Forum from American Express -- where small business owners can get advice from experts and share tips with each other.

The U.S. Small Business Administration (SBA) has had a tough couple of years. A combination of tighter credit standards among its authorized lenders, a lack of secondary market options for its loans, and depressed borrowers have made it tough for the them to help businesses through the credit crunch. But thanks to American Reinvestment and Recovery Act (ARRA) initiatives, the first quarter of 2010 shows weekly SBA loan volume up 90% over comparative weeks in 2009.

The SBA received an initial $730 million to help small businesses from ARRA last February. About half of that ($375 million) went toward increasing the guarantee on the SBA's most popular loan programs and to waive borrower fees. The whole idea was to encourage banks to loosen the purse strings on small business lending.

The strategy seems to have worked. While SBA guaranteed loans were down 36% in 2009, ARRA successfully kick-started lending to such a degree that by November 2009, the funds were exhausted. Since then another $225 million has been allocated, including the latest infusion of $40 million last Friday.

About 44,000 companies received 7(a) loans in 2009. The average loan totaled $210,000. Women and minorities accounted for 15% and 25% of borrowers, respectively. About a third of the funds went to startup businesses. Microloans, a relatively new offering, averaged $12,000 each; 966 such loans were extended in 2009.

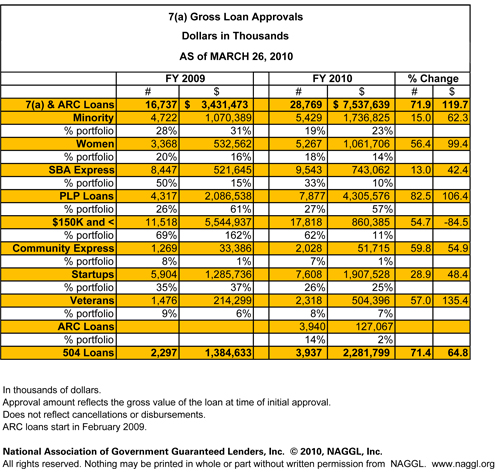

The National Association of Government Guaranteed Lenders (NAGGL) offers a peek at SBA lending activity from October 1 through March 26 of 2009 versus 2010 (their fiscal year ends September 30)*.

How to Get an SBA Loan

Contrary to popular belief, the SBA does not make direct loans. Instead, they encourage bank and non-bank lenders to make loans they otherwise wouldn't by offering a guarantee in the event of default. Currently that guarantee is for up to 95% of the loan.

Also contrary to popular belief, in most cases, it doesn't take any longer to get an SBA loan than it does to get a regular business loan. In fact, the information an SBA lender requires, save for a few extra details, is the same as for regular loans.

By far, the most active SBA loan program is what's called the 7(a) Program. They can be used for working capital, equipment, and business real estate (though an SBA 504 loan may be a better choice for the latter). Loans can be used fund start-ups, business purchases, franchises, and occasionally debt replacement — especially in times of economic difficulty.

7(a) loans generally offer 7- to 25-year repayment terms for real estate and equipment, and up to 7 years for working capital.

The lender requires about 20-25% of the total financing to come from you, but that can include all of the expenses including the "soft costs" (e.g. architectural plans, moving expenses, etc.).

You and anyone who owns more than 20% of the company will be required to personally guarantee the loan (along with spouses), and you'll probably be required to pledge your home as collateral — but these conditions apply to almost all small business borrowing.

The SBA sets maximum rates and fees for its guaranteed loans. While they're subject to change, for loans over $50,000 with terms of 7 years or less, you'll probably pay Prime + 2.25 percent. For loans with longer maturities, you'll pay Prime + 2.75 percent. Smaller loans will be priced higher. Both your lender and the SBA may charge an up-front fee of about 2 percent, but in troubled times this may be waived or reduced.

How to Find an SBA Lender

Your local SBA office can provide a list of their authorized lenders. Here are the ten top SBA lenders (by volume of loans) in 2009 from NAGGL's website (full list download):

- Superior Financial Group, LLC (Walnut Creek, CA): 2,690 loans totaling $27,177,500

- Wells Fargo & Company (San Francisco, CA): 2,156 loans totaling $678,221,500

- U.S. Bank (Minneapolis, MN): 1,896 loans totaling $261,602,982

- Zions Bancorporation (Salt Lake City, UT): 1,310 loans totaling $128,213,000

- JPMorgan Chase & Co (New York City, NY): 1,250 loans totaling $136,576,000

- Innovative Bank (Oakland, CA): 1,016 loans totaling $56,011,700

- Huntington Bancshares Inc. (Columbus, OH): 992 loans totaling $141,398,400

- Citizens Financial Group, Inc. (Providence, RI): 709 loans totaling $40,394,500

- Manufacturers & Traders Tr Co (Buffalo, NY): 692 loans totaling $72,963,475

- Compass Bancshares, Inc. (Birmingham, AL): 615 loans totaling $171,617,500

Don't assume that because one SBA lender isn't interested in your loan, none will be. Each lender has their own approval criteria and some prefer certain types of deals to others. Just be sure to tell your lender if you've already been declined. They will find out anyway, and it will look bad for you if you didn't tell them.

More than 1,200 lenders that haven't made an SBA loan since 2007 are now back in the game. There's probably never been a better time to tap the SBA. They're eager to help jumpstart the economy and hey, they're part of the organization that prints the money.

For more information on all of the SBA loan programs, a directory of their regional offices, and other useful links, visit the SBA's website. For other advice about SBA loans and other financing options, visit Finding Money Advice.

*Chart published with permission.

Disclaimer: The links and mentions on this site may be affiliate links. But they do not affect the actual opinions and recommendations of the authors.

Wise Bread is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to amazon.com.