The First Step to Budgeting

Why do so many budgets fail? Because the first step to budgeting is omitted. When implemented correctly, it can make a huge difference. When the first step is neglected, intangible and unrealistic budgets are often created — a recipe for disaster.

So, you ask, what is the first step to budgeting?

Keeping Track of Expenses

It’s that simple. But it still requires a process, which is described below.

Once you decide you want to create a budget, you need a starting point. You can’t accurately and immediately forecast what you will spend in the future if you have no historical frame of reference to work with.

The Idea

Right off the bat, all you need to worry about is simply keeping track of your expenses. You don’t judge yourself (or your partner if you are doing this together) for what you are spending. Simply keep track.

You may notice that just as a function of keeping track of your expenses, you already become more budget-conscious and will spend less anyway. But don’t beat yourself up if that doesn’t happen. Just keep track of what you spend — religiously.

Yes, those little cups of coffee count too. Record. Everything.

Format

Using a spreadsheet to keep track of your expenses is best, since it makes for easy calculation of expenses and viewing of running totals at a glance.

However, you may not always be in front of your computer, so use whatever means you need to remember/record each day’s expenditures. You can either sit down to your computer at the end of every day and do it, or keep a notebook handy and record your daily expenses so you can update the spreadsheet every few days.

You can, of course, choose to exclusively use a notebook instead. However, it will be more difficult to analyze your expenses as each month progresses and use it as a barometer for how you are doing. It’s possible, but requires more active and repetitive calculator work.

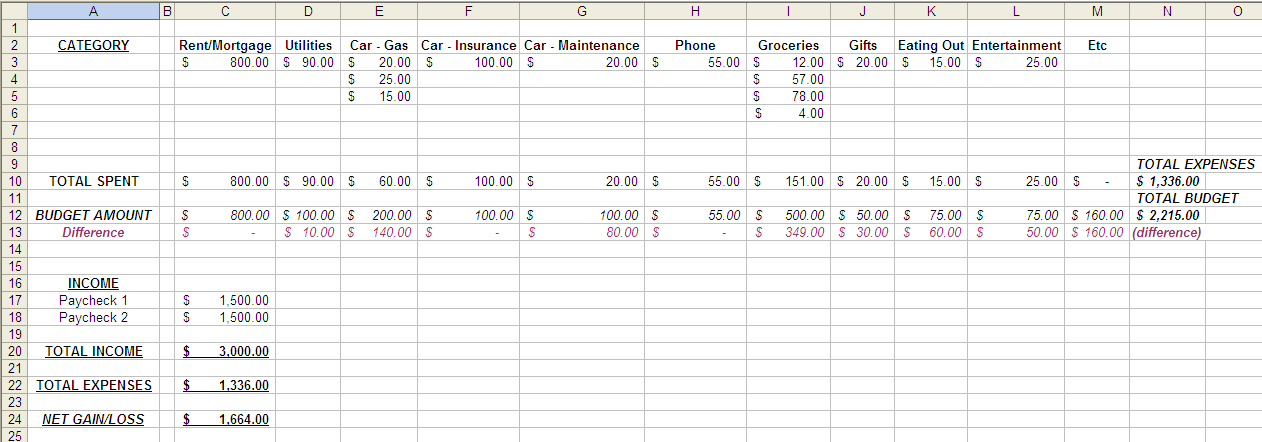

Pictured above you will see a very basic sample spreadsheet format for keeping track of your expenses. You create the categories along the top as you see fit and as fits your lifestyle, and each time you spend money within those categories, you list the expense. A few rows down, a line of running totals indicate you how you are doing.

If you need more room to list your expenses under a certain category as the month rolls on, just add more rows and keep listing.

If you wish, feel free to add extra columns to add the date of each expenditure. It’s up to you.

At the End of Month One

Once you have a month of expenses recorded, take a look at how you fared.

- What did you spend in each category?

- Do you feel it was a typical spending month, or were there unforeseen circumstances that altered the outcome?

- What is an average spending amount that will work for you?

- Are you surprised by any of these spending amounts?

- Are there any spending habits you want to change right away?

Now it’s time to add another row to your spreadsheet: a budget row. Certain fixed expenses will be easy to budget for; others will fluctuate and require some flexibility. Don’t worry about these numbers needing to be perfect right away; think of this row as a work in progress.

Month Two

Start with a fresh spreadsheet, and keep recording your expenses every day. (This will ideally become a force of habit that will last for months, so get used to it). This month, as you record your expenses, check your running totals against your budget amounts to see how you are coming along as the month goes by.

As you do this over time, you may find that you’ve tapped out your Entertainment budget early on in the month. With this knowledge, you will either reconsider going out again, or will find money from another category of your budget that you anticipate under-spending on this month for some reason. This is your budget — you get to control how it goes down; keeping track of your expenses is a mechanism for ensuring you spend within your means.

Spreadsheet Extras

Once you start playing with budget amounts, you may also want to insert useful columns for income so you can see how much you are spending versus saving. Pictured here you will see a fuller sample budget spreadsheet, part way through a month:

Ensuing Months

Continue keeping track of your expenses as you have been doing, and if needs be, continue to edit your budget amounts. No two months are the same, and you won’t have a solid budget after only two months. For example, many people find that the upcoming holiday season wreaks havoc with their budgets. Use the flexibility in your own budget to ensure that you stay on track, possibly by finding other areas where you can cut back to compensate.

The Second Step to Budgeting

Guess what? You can stop at the first step if you like. Why? Because by keeping track of your expenses, you have unwittingly created your entire budget. Congratulations!

Simply continue to keep track of your expenses, record income and tweak budget amounts to make sure your finances balance out the way you want them to each month.

Additional photo credit: Nora Dunn

Disclaimer: The links and mentions on this site may be affiliate links. But they do not affect the actual opinions and recommendations of the authors.

Wise Bread is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to amazon.com.

{kind=link}

While keeping track of expenses is an important part of creating a budget, I disagree that it is the first step. In my mind, the first step is creating goals. Without goals, the budget has little meaning, and can feel restricting. With goals, the budget takes on meaning. Committing to the goals means you will commit to the budget.

For example, "I want to go to Paris next year" is a goal; now you have a reason to budget enough money to make that dream a reality.

Even "I don't want to overspend my paycheck," or "I want to get out of debt" are goals.

It's important to have a reason to budget before you even begin the process.

Brian you are correct. Without a person setting his/her goals then he/she will have nothing to budget for.

You have correctly identified the main reasons why a lot of budgets don't work!

I could not function without Google Docs at this point - I hack my entire life. But I think the people above have a good point. Not everyone is into recording minutia. Some people are "big picture" people. I don't understand them much because I'm a crunch-the-numbers person but they do exist. There are always multiple solutions to personal problems.

That said, I wholeheartedly am for recording every single penny of income and expenses. I have been doing this since Jan. 1 this year and I LOVE the ability to analyze my expenses. Since I have everything in (Google) Excel, I can make all manner of graphs, see how my spending has changed from month to month in every single category. For instance, of all my expenses, 7% this year has gone to "vacation." That blows me away but I have to say my vacations have been some of my favorite parts of the year... it's probably totally worth it.

It's awesome to KNOW where my money is going as opposed to having a HUNCH.

Nice round up of the basics of budgeting. I do agree with Brian (1st comment) in that it's good to have a goal, something you're working towards. Maybe it's a fully-funded emergency fund, a vacation, a major purchase. Budgeting ultimately means saving, and having checkmarks along the way makes a huge difference.

I was so glad to see this post. Some people just don't know where to begin. While I agree a spreadsheet can be effective, there's a new Web site that will do it for you--and save information over time to track changes. It's http://www.debtspark.com. It gives you a quick, clear snapshot of income, debt and expenses. It's very easy to use and helpful for starting off this daunting process.

It works fine to just pick categories out of thin air--setting them up however seems to make sense to you. But you can do better than that.

If you've got a working budget, I wouldn't suggest mucking around with your categories for some theoretical gain. But if you're creating a new budget (or if you're changing around your budget categories for some reason of your own), I've got some suggestions on what makes a good category.

In writng down what we actually spend, we realize the stuff that's most important (but not as immediate) often gets shoved aside. So the first poster had a good point. Because "a little leak sinks a big ship", I think Nora's process works for most of us. It's like untangling a ball of thread, you can start at either end. The point is just do it.

Thank you all for the comments! Great discussion.

The article was inspired because I introduced this concept to a friend recently who needed to start budgeting, and now he talks almost evangelically about his new budget! For him, a simple awareness of where his money goes made all the difference.

@Brian - I agree completely that setting goals is the first step. I guess I didn't include it as the first step to budgeting, because I believe that goal-setting falls into the more general financial planning arena. But I do agree: a budget is all but useless without goals.

Thanks to @kerri for the link to DebtSpark, and to @Philip for the complementary article.

To everybody else, thank you for your input! Keep it coming...

Another great budget tracking tool is Mint.com. It is free and easy.

I love using Mint because it automatically downloads my bank account information and email's alerts when you have gone out of your budget.

Once a month, I log onto my online banking website, fire up my budget in Excel, and then split my desktop vertically between both windows. I then scroll through my transactions over the previous month on my banking website while tallying the amounts in each category in my spreadsheet.

This means I don't need to keep receipts or record transactions daily, which is far more time efficient and easier to maintain. Just set a monthly reminder if you are forgetful, like me.

The only downside is I cannot keep track of my spending when using cash, but I use my debit or credit card for most things. Cash is used primarily for food, like vending machines and coffee, so that is how I categorize it.

Keeping track of every expenditure is excruciating. It's fun at first because your budget is a new project, but after a while, you know what your lifestyle requires.

How about this -- three steps:

(1) Track all your expenses for 3 typical months. Then you know about what you spend on incidentals -- things that occur over and over and are part of everyday life. Food, gas, dry cleaning, meals out, entertainment, etc.

(2) Add up your monthly bills -- things you don't need cash for, things that don't pop up. Your mortgage / rent, insurance, cable, internet, phone, utilities, homeowners' fees, taxes, student loans, charitable contributions, etc. Only include things that you need every month like clockwork.

(3) Go through your whole life and figure out those things that happen once or twice a year -- things that surprise you. Car insurance. Magazine subscriptions. Parking tickets (well, 3-4 times a year for me). Your license plate renewal. Christmas / holiday gifts. Your flight home for Thanksgiving.

Now, how to manage all this? Take the amount you come up with in (1), add 10 percent as a buffer, and have it direct deposited into your checking account. Pretend that this is all the money you have available for the month, week, whatever.

Then, take (2), add a little buffer, and put it into some online account that you can pay bills from every month.

Take (3), add it all up over the year, divide by your number of paychecks, and add that to a savings account at each paycheck - preferably with direct deposit. Only draw on the savings account as you need it to pay for your annual events. It's a good idea to include an allowance for car repair, maybe a new phone, computer, whatever you have planned for the year.

THanks for the comments about your budgeting systems, people! This is great, because everybody has a different system that works for them. WHat might be easy to me could be excruciating to another person.

I really like the total system Guest above has outlined. It's true: after about 3 months of tracking your expenses, you have a good sense of where your money goes. Throwing in the intangible expenses and organizing what gets paid from where is an excellent way to streamline the process.

Here's another way to budget for those irregular expenses that can throw you off:

http://www.wisebread.com/budgeting-hack-gift-calendars

Agree with most of the comments but mostly with Brian.

While Budget, and good budget systems is fantastic, it is of no value if the there are no set goals.

If by goal is to pay of debt then my budget should reflect this goal. Once specific goals/milestones within the budget are met, then the the budget should be adjusted to reflect the current position.

It's interesting how my personal life is often reflected in the articles I write for Wise Bread. You see, I'm doing this very exercise right now along with my boyfriend. What I didn't realize (possibly because it is a natural process for me) is that it came about as a function of having first developed a very specific savings goal. And because we are motivated by our goals, the budgeting part is actually providing us with continued inspiration to persevere.

So kudos to Brian and others for observing that goals are truly the first step to budgeting. Thanks!

Your blog is full of interesting articles, thanks for good read

Very interesting blog, bookmarked for the future referrence, what template do you use ?

I totally agree that tracking expenses is the key to budgeting. That was the focus of my last article for the Vancouver Voice. You do a great job covering the issue.

@Tim - Thanks! Although the effort required to track expenses is why so many budgets fail, it is truly the first step to becoming financially aware. If people aren't prepared to track their expenses, then I would argue that they don't want to create a budget badly enough.