Feed items

The sunny side of pessimism

From the Declaration of Independence to the space program, optimism was traditionally something of a core American value; however, it is one that has taken quite a beating in recent years.

Not too long ago, an NBC-Wall Street Journal poll found that 76 percent of Americans lack confidence that their children will have a better life than they do. That is a stunning reversal from the onward-and-upward America in which baby boomers were reared. Then again, the optimism of the baby boom generation atrophied into a dangerous complacence which has been bad for the economy in general and for household finances in particular. The following are some examples of how this complacence has led to trouble, and why the new mood of pessimism might actually be constructive:

“Thinking Money” a rich change of pace from TV’s wasteland

Have you ever wondered why your next-door neighbor must have a new car in his driveway every model year?

And not just a new car, but a new car with all the bells and whistles, like that 18-valve, turbo-charged, dyno-flex, hydroponic 4000 engine, 57-speaker audio system with Sistine Chapel acoustics and the buttery soft leathers imported from recently-discovered islands off the Madagascar coast?

It turns out he is just giving in to the inclinations that characterize too many American big spenders, who gain their greatest joy from acts of overspending.

That’s right, many humans are simply pre-programmed to overspend, an action that illuminates the pleasure centers of their brains. To these people, saving lacks sex appeal. It is spending, not saving, that is sexy.

“Thinking Money” a rich change of pace from TV’s wasteland

Have you ever wondered why your next-door neighbor must have a new car in his driveway every model year?

And not just a new car, but a new car with all the bells and whistles, like that 18-valve, turbo-charged, dyno-flex, hydroponic 4000 engine, 57-speaker audio system with Sistine Chapel acoustics and the buttery soft leathers imported from recently-discovered islands off the Madagascar coast?

It turns out he is just giving in to the inclinations that characterize too many American big spenders, who gain their greatest joy from acts of overspending.

That’s right, many humans are simply pre-programmed to overspend, an action that illuminates the pleasure centers of their brains. To these people, saving lacks sex appeal. It is spending, not saving, that is sexy.

Retirement planning for women: Strategies for a secure retirement

- More than two-thirds (68.1 percent) of the elderly poor are women.

- An October 2012 study by the American Association of University Women found that over the course of a 35-year career, an American woman with a college degree will make about $1.2 million less than a man with the same education.

- More than 70 percent of nursing home residents are women, whose average age at admission was 80. In 2006, the average annual cost of a private room in a nursing home was $75,000 and a shared room almost $67,000.

- It is a well known fact that women live longer than men.

- A 2010 survey by Transamerica Center for Retirement Studies shows that just 8 percent of women feel they are already educated enough to successfully reach their retirement savings goals.

Where am I going with listing all these statistics? Women need to take their retirement planning seriously.

Retirement planning for women: Strategies for a secure retirement

- More than two-thirds (68.1 percent) of the elderly poor are women.

- An October 2012 study by the American Association of University Women found that over the course of a 35-year career, an American woman with a college degree will make about $1.2 million less than a man with the same education.

- More than 70 percent of nursing home residents are women, whose average age at admission was 80. In 2006, the average annual cost of a private room in a nursing home was $75,000 and a shared room almost $67,000.

- It is a well known fact that women live longer than men.

- A 2010 survey by Transamerica Center for Retirement Studies shows that just 8 percent of women feel they are already educated enough to successfully reach their retirement savings goals.

Where am I going with listing all these statistics? Women need to take their retirement planning seriously.

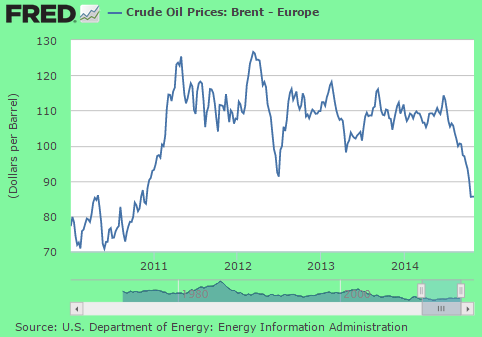

Why lower gas prices are fleeting

If you didn’t hear it on the news, you probably noticed it the last time you filled up your car: gasoline prices have been dropping lately after holding fairly steady for a year or so, following world oil prices.

After clicking your heels at the gas station when nobody was looking, you probably got in your car and started wondering: Is this for real? How long can it last? Is this just one of those blips you can clearly see on the chart, or are we seeing a fundamental shift toward lower energy prices? If lower energy prices sound like a dream, that’s because, in our lifetimes, we’ve only see them go up. However, the notion of a long-term drop in energy prices may not be so totally far-fetched.

Three mega-trends could account for the drop:

1. Natural gas

Why lower gas prices are fleeting

If you didn’t hear it on the news, you probably noticed it the last time you filled up your car: gasoline prices have been dropping lately after holding fairly steady for a year or so, following world oil prices.

After clicking your heels at the gas station when nobody was looking, you probably got in your car and started wondering: Is this for real? How long can it last? Is this just one of those blips you can clearly see on the chart, or are we seeing a fundamental shift toward lower energy prices? If lower energy prices sound like a dream, that’s because, in our lifetimes, we’ve only see them go up. However, the notion of a long-term drop in energy prices may not be so totally far-fetched.

Three mega-trends could account for the drop:

1. Natural gas

In praise of not planning

It’s a good thing that I am a planner by nature because, dealing with personal finance as I do involves a lot of long-term planning. So it might seem a little odd for me to take this position, but there are times when your finances might be better for not having made a plan — or at least for not being completely ruled by your plans.

Don’t take this too literally because planning has its place, but planning can also become tyrannical. It intimidates people from undertaking projects. Once a project is undertaken, too much reliance on planning can make people blind to better alternatives.

So the message here is don’t let planning become obsessive. The following are some examples of when freedom from planning can come in handy:

In praise of not planning

It’s a good thing that I am a planner by nature because, dealing with personal finance as I do involves a lot of long-term planning. So it might seem a little odd for me to take this position, but there are times when your finances might be better for not having made a plan — or at least for not being completely ruled by your plans.

Don’t take this too literally because planning has its place, but planning can also become tyrannical. It intimidates people from undertaking projects. Once a project is undertaken, too much reliance on planning can make people blind to better alternatives.

So the message here is don’t let planning become obsessive. The following are some examples of when freedom from planning can come in handy:

Zeroing in on target-date funds

For those investing for retirement, target-date funds sound like a great idea. Say you want to retire in 2030. Simply purchase a 2030 target-date fund, the wisdom holds, and the fund will do a lot of the heavy lifting for you when it comes to your investments.

But like that time you tried to pass your literature midterm by scanning the Cliff’s Notes of “Crime and Punishment,” taking the easy way out may not be your best strategy here either. As one expert says, target-date funds are “the one-stop shop for mutual fund investing.” In selecting the holdings comprising the fund, target-date fund managers choose a higher concentration of high-risk, high-return holdings in early stages, gradually converting to lower-risk holdings as the target date nears.

{kind=link}

Facebook

Become a fan

Twitter

Follow us

RSS

Subscribe