Among the Wise Bread community, I get the sense that there's a kind of "pox on both their houses" attitude to the problems in the subprime mortgage markets. People who worked through their own credit problems (or avoided having any) can't stir up much sympathy for people who bought houses they can't afford--and pretty much nobody has any sympathy for the mortgage brokers and hedge funds that lent them the money. A new guide from Americans for Fairness in Lending, though, shows that the damage actually hits at every level, from the individual borrowers (including borrowers with good credit), through the neighborhood, local economies, and the national economy. With their kind permission, we're presenting the guide here on Wise Bread.

The study is Neighborhood and Individual Impact of the Subprime Mortgage Lending Crisis: A Reporter’s Guide and has two parts.

The guide lists half a dozen negative impacts that the crisis has had on borrowers and the economy. Among them are:

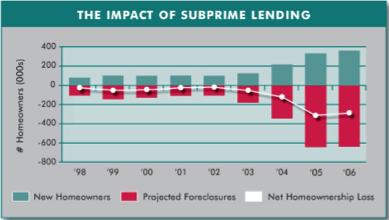

Loss of homeownership One of the supposed benefits of subprime lending was that it made homeownership a possibility for people who had been shut out. It turns out that, because many of these loans didn't go to first-time homebuyers, the result has been an actual reduction in number of homeowners.

According to the Center for Responsible Lending, “Subprime loans made during 1998-2006 have led or will lead to a net loss of homeownership for almost one million families.â€

Weakening Property Value The crisis is pushing down property values in multiple ways. People who can't afford their mortgage are putting their homes on the market--either voluntarily or through foreclosure. Plus, as the crisis makes it harder to get a mortgage, there are fewer buyers--putting downward pressure throughout the housing market.

Homeowners who took subprime loans are not the only ones impacted by the crisis. It is estimated that each foreclosure lowers the property values in its neighborhood by about one percent.

Damaging Neighborhood and National Economies More money going to money center banks and hedge funds means less money going to local business. Rising numbers of economically troubled families has ripple effects throughout the local economy.

The Center for American Progress notes that foreclosure is more than an individual tragedy: “A spike in foreclosures can also create a domino effect in a single area, leading to a sharp depreciation in property values, decreased business investments, and lower tax revenues, which in turn affect the quality of schools and decrease nearby property values.†Stores such as Home Depot and Wal-Mart are reporting reduced consumer spending in the wake of the meltdown, resulting in a loss of tax revenue. Counties are reporting losses in revenue from filing and tax fees. Property values are decreasing, yielding even greater losses for local communities in tax revenue.

Part one ends with some policy suggestions for fixing the problem, including help for homeowners stuck in troubled loans, laws against predatory lending practices, and incentives for lenders to come to the table to work out problem loans.

Part two provides a look at how we got here, and has a pretty good explanation of the changes in the way mortgages loans were made and what happened to them afterwards. It also takes a look at the question, "How do the lenders make any money loaning money to people who can't pay it back?" The answer has to do with the incentives at each layer in the process.

Subprime loans are generally made through brokers and with some lenders, loan officers who, despite popular perception, are under no obligation to find the borrower the best rate...or even a loan they can afford. On the contrary, the commissions of brokers and loan officers increase based on loan size and the interest rate charged....

Subprime lenders immediately dispose of the loans they write by packaging them for quick sale to Wall Street investors. Lenders make their profits up front, from the sales of those loans and the fees they pack into each mortgage...

Until very recently, when the loan volume grew so large and default rate skyrocketed, Wall Street investors were generally insulated from the impact of bad subprime loans. The loan portfolios pooled risky subprime loans, reducing the chances that a small percentage of defaulting loans would hurt the bottom line.

As you might expect from the name, Americans for Fairness in Lending is an advocacy group that works to protect consumers from abusive lending practices, and the guide is written from that perspective. I expect you'd get a very different analysis from an association of mortgage brokers or bankers. With that caveat, Neighborhood and Individual Impact of the Subprime Mortgage Lending Crisis: A Reporter’s Guide is an excellent overview of the situation and is well worth reading.

Disclaimer: The links and mentions on this site may be affiliate links. But they do not affect the actual opinions and recommendations of the authors.

Wise Bread is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to amazon.com.

{kind=link}

And it also doesn't help that you have self interested groups that continue to

hype the real estate market. The subprime mess has really dragged many lives and households into the hole.

So, I just got an offer to refinance from Countrywide Home Loans, who suggest that I change my mortgage to a 40-year loan. Can you imagine? They also addressed the letter to "A. Andrea". SOMEBODY didn't learn how to use mail merge properly.

I actually do feel very sorry for people who were hoodwinked into taking out mortgages that were too much too handle. I can see how easy it would be.

Also, the practice of bundling and reselling all kinds of loans and insurance to Wall Street strikes me as increasingly common - I wonder if any other industry is going to face the kind of drama that subprime is facing now?

Your article let me have a clear picture of the subprime loan crisis. Thanks you very much.

Great article you have here. Its effect is a big-big global one. The stocks sentiments on this issue...

What an excellent read and shed light to the crisis and where things are heading. I presently live in southern Ontario, Canada but have a brother working in the mortgage industry in FL. I've heard nothing but whining from him for a while now but because I'm not living there anymore, wasn't really privvy to what was truly going on. I'm going to send this article to him and see what he has to comment. Now I have to wonder where he stands with things...whether he thought he could make a quick buck or if he's innocent and unknowing in all this. Thanks for the GREAT article!

Mary

Jack Guttentag (a former finance professor at the Wharton School of the University of Pennsylvania) also offers insight and suggestions for dealing with the subprime crisis, which I found interesting. Much of the crisis, in his opinion, is associated with the "end of house price appreciation" rather than subprime lending itself.

Some readers may remember a less impactful subprime crisis in the late 1990s dealing mainly with manufactured housing/lending/securitization. Standard & Poor's has an interesting article comparing current events with the bankruptcies of Conseco and Oakwood Homes.

These things always happen in cycles. Once everything blows over, you will see new lenders showing back up slowly, however, they will not be so aggressive this time.

I really appreciated your article on how the subprime crisis affects even those who weren't sold these types of mortgages. I have become a victim of the things described in Part One of your post.

Just on our street, there are 3 vacant bank owned homes that are not being maintained and decreased the value of the rest of our homes in the neighborhood.

Sadly, I also feel prey to Part Two of your post in 2005. I recently wrote about how I was sold an interest-only loan and the background on the housing market. Thankfully, we are not in over heads and we are one of the few whose income caught up with our mortgage.

I think your information is informative and can help new borrowers be aware of the potential danger of purchasing subprime mortgages.

I saved 7 years for the house I bought in Plymouth, MI, and put down $40,000 (10%) at signing. I also went for a 30 year mortgage even though I was presented with 5 options that included subprime lending practices. I had to actually request a 30 year mortgage.

According to the prices houses are being sold for in my neighborhood, I can expect my house to sell for $100,000 less than I bought it for. What about the people who acted responsibly? What is the government going to do for us? If homeowners who were irresponsible are bailed out, what are they going to do for me? I will need to move to another state in a year and I will most likely end up in an apartment owing money on this house. I am so angry right now. I feel as though I am going to lose everything.